Redacción Alabrent

There are several factors underlying this reversal of the trendFirstly, the numbers for 2022 follow the two disruptive and volatile years 2020 and 2021, when peaking label demand was heavily influenced by excess demand for essential goods and services after the outbreak of the pandemic in 2020, and by rapid economic recovery in 2021.

Supply chain distortions

Secondly, since the summer of 2021, global manufacturing chains have been suffering from supply chain disruptions caused by Covid-related adjustments. This led to a growing gap between booming post-Covid demand and the shrinking availability of energy, raw materials, components, chemicals, production, labour and transport capacity.

In the first half of 2022, the European label industry was particularly hit by the long lasting strike at UPM, a leading paper manufacturer in Finland. Not only did this limit the availability of facestocks for paper labels, but more importantly, a significant share of raw materials supply for paper-based release liners (the siliconized materials carrying the labels) was cut off from the market for more than 100 days.

In the first quarter of the year, the effect was dampened by significant inventory surpluses that had been built up in the final quarter of 2021 in anticipation of further increases in lead times and raw materials prices. However, in the second quarter output was severely hit with lead times going up to 5-6 months and label converters being served on allocation. Part of the decline in paper label consumption may have been absorbed by increases in filmic label demand.

In the latest FINAT RADAR, the association’s 6-monthly market survey, it was reported that 60% of participating converters, surveyed this spring, had been suffering revenue losses as a result of supply chain issues. Although the strike finished just before Easter, it is expected that backlogs will not be filled before this autumn.

Recession outlook

Thirdly, by that time, supply side related constraints may have been overtaken by demand factors, with exponential increases in energy prices, raw materials costs and, ultimately double digit consumer price inflation eating into disposable incomes and consumer spending, and the dark clouds of the horrific war in Ukraine not expected to clear anytime soon.

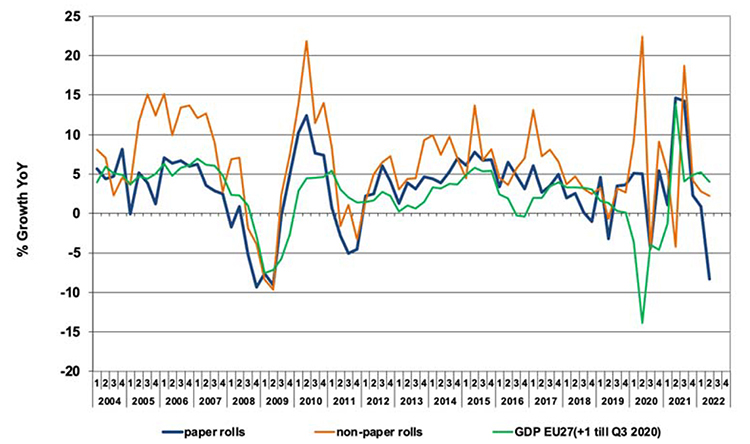

As reported previously, statistically, demand for self-adhesive roll label materials is a significant indicator of European GDP. Although the correlation between the two has been distorted somewhat by the volatile consumption patterns during the ‘Covid years’, part of the downturn points at an economic shift in Europe in the months to come.